You are now leaving Meeder Investment Management. Links to other websites are provided for your convenience and information only. When you click on a link to another website you will be leaving this website. The fact that Meeder Investment Management provides links to other websites does not mean that we endorse, authorize or sponsor the linked website, or that we are affiliated with that website’s owners or sponsors. This material is being provided for informational purposes only and is not a solicitation or an offer to buy any security or to participate in any planning or investment strategy. Unless otherwise indicated, the linked sites are not under our control and we are not responsible for and assume no liability for the content or presentation of any linked site or any link contained in a linked site, or any changes or updates to such sites. We make no representations about the accuracy or completeness of the information contained in any linked sites and their privacy and security policies may differ from ours. We recommend that you review this third-party’s policies and terms carefully.

Despite expectations of imminent rate cuts, Federal Reserve Chair Jerome Powell emphasized needing additional evidence indicating a stabilization of inflation before contemplating any policy easing, thereby contributing to an increase in volatility of U.S. Treasuries. Abroad, concerns surrounding China’s economic performance acted as a drag on the Emerging Markets index, which concluded the month down -4.6%. Meanwhile, the 10-year U.S. Treasury yield saw a slight uptick, climbing from 3.9% to 4%, consequently nudging U.S. investment-grade bonds into negative territory.

February showcased the resilience of U.S. equity markets, with the S&P 500 delivering an impressive surge of +5.34%. Smaller market caps represented by the S&P MidCap 400 Index and the Russell 2000 Index also demonstrated positive momentum. This improvement helped equity markets extend the rally with increasing market breadth.

Fixed-income investments faced significant headwinds. The Bloomberg US Aggregate Bond Total Return Index suffered a decline of -1.41% in February. This downward trajectory was attributed to persistent upward pressure on interest rates and lingering concerns surrounding inflation. On the global front, emerging market equities exhibited signs of improvement, while developed international stocks posted relatively modest gains, underscoring the contrasting performance between domestic and international equities.

March provided mixed economic data, presenting investors with a blurred picture of the economic landscape. The ISM Manufacturing PMI provided hope by surpassing consensus estimates to reach 50.3, marking the first monthly expansion since September 2022. The S&P 500 surged to a new closing high, reaching 5264 by the end of the first quarter. The S&P 500 extended its quarterly gains to +10.5% as eight of eleven sectors were positive.

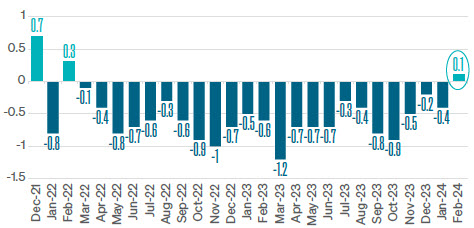

Data for Leading economic indicators, as measured by the Conference Board Leading Economic Index (Exhibit 1), climbed higher for the first time since February 2022. Investors welcomed this positive news because the LEI provides early signals of economic turning points in the U.S. business cycle.

In the first quarter of the year, the market’s upward momentum from the end of 2023 persisted, with the S&P 500 Index reaching multiple record highs and delivering a robust return of +10.5%. The market rally broadened as mid-cap stocks represented by the S&P 400 Index grew nearly 10%. This contribution helped 8 of 11 S&P sectors post positive performance. Investors in portfolios utilizing the Meeder Growth Strategy experienced increased volatility than some of the others in our suite of risk-based portfolios, however, those who remained invested earned the highest investment performance.

The Meeder Investment Positioning System (IPS) model, began the quarter with a 95% allocation to stocks. Riding the momentum of a strong market finish in 2023, all ten trend and momentum indicators within the short-term model were positive. As January progressed, discussions of a “soft landing” for the U.S. economy bolstered optimism in the intermediate-term model, despite expectations of a slowing economy in 2024. By January’s end, investor optimism remained profound, which we view from a contrarian perspective. The short-term model reflected strong trends and momentum, against the backdrop of above-average valuations and elevated interest rates that weighed on the long-term model score.

In February, as market breadth waned, the short-term model retained positivity, while expectations of multiple Fed rate cuts in 2024 prevailed. A combination of strong longer-term market trends and improvement in industry-level market breadth led to the long-term model’s most positive reading in nearly 2 years. Bullish market sentiment weighed on the intermediate-term model score, from a contrarian perspective.

By March, the market reached new highs and the short-term model maintained its positive strength. The intermediate-term model score improved as bearish options activity increased following a reversal in investor sentiment. The quarter concluded with the short-term model showing strength. The intermediate-term model reflected positive expectations around Fed rate cuts, and the long-term model remained neutral due to lingering concerns over elevated valuations leading us to end the quarter with 96% exposure to stocks.

As February unfolded, we continued to capitalize on the prevailing market conditions. Amid expectations of delayed Federal Reserve rate cuts and robust economic growth, we maintained our overweight position in U.S. high-yield bonds, capturing the attractive yield premium and capitalizing on the potential for substantial economic growth. The Strategy adjusted its duration to lower than the benchmark, anticipating shifts in interest rate expectations. We remained neutral on our emerging market debt allocation but made incremental adjustments to its exposure in response to evolving volatility, currency dynamics, and market momentum.

In March, the Fed provided additional guidance and pushed rate cut expectations further into the future. Volatility declined in emerging market debt and price momentum increased. Therefore, we increased exposure to emerging market debt while maintaining its overweight stance on U.S. high-yield. These adjustments highlighted the Strategy’s flexibility to capitalize on near-term opportunities while navigating evolving macroeconomic market dynamics. We remained vigilant in managing its duration, ensuring alignment with market expectations, and preserving its risk profile amidst changing interest rate scenarios. Overall, the shifts throughout the first quarter of 2024 demonstrate the Meeder Fixed Income Strategy’s adaptability and commitment to optimizing portfolio performance in dynamic market environments.

©2024 Meeder Investment Management, Inc.

0107-MIM-4/15/24-41950