You are now leaving Meeder Investment Management. Links to other websites are provided for your convenience and information only. When you click on a link to another website you will be leaving this website. The fact that Meeder Investment Management provides links to other websites does not mean that we endorse, authorize or sponsor the linked website, or that we are affiliated with that website’s owners or sponsors. This material is being provided for informational purposes only and is not a solicitation or an offer to buy any security or to participate in any planning or investment strategy. Unless otherwise indicated, the linked sites are not under our control and we are not responsible for and assume no liability for the content or presentation of any linked site or any link contained in a linked site, or any changes or updates to such sites. We make no representations about the accuracy or completeness of the information contained in any linked sites and their privacy and security policies may differ from ours. We recommend that you review this third-party’s policies and terms carefully.

» Federal Reserve Raises Rates

» U.S. Economy Still Strong

» Inflation Eases as Consumer Debt Increases

The credit agency provided two positive factors that led to their stable outlook for the United States. The U.S. maintains the world’s most powerful economy, with an output of more than $20 trillion in GDP. The second factor is that the U.S. dollar remains the world’s primary reserve currency. This status allows the U.S. government exceptional flexibility to finance its activities.

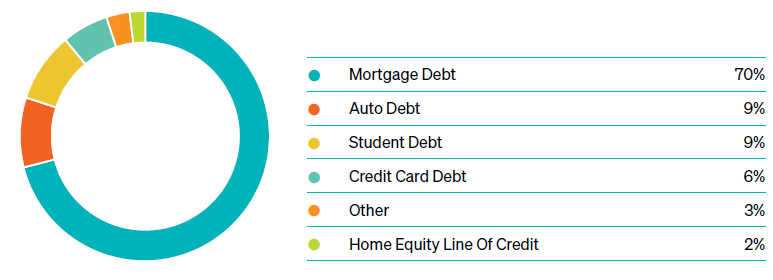

The vast majority of this total is mortgage debt and remained steady. However, auto and credit card debt increased $20 and $45 billion, respectively, over the quarter. The 4.5% increase in credit card debt pushed the balance to $1.03 trillion and exceeded the trillion-dollar threshold for the first time in history. Bankrate recently found that 47% of credit cardholders carry debt from month to month, up from 39% in 2021. Even more troubling is the fact that 60% of Americans with credit card debt have had it for at least a year, up 10 percentage points from two years ago.

An essential factor to remember when evaluating the financial health of the U.S. consumer is that the repayment of federal student loans has paused since the global pandemic. Payments on these loans are scheduled to restart in October and balances are now equivalent to auto debt as the second most significant component of total consumer debt. It will be interesting to see if student loan repayment hurts consumer spending, as this metric accounts for nearly 70% of the U.S. GDP.

Commentary offered for informational and educational purposes only. Opinions and forecasts regarding markets, securities, products, portfolios, or holdings are given as of the date provided and are subject to change at any time. No offer to sell, solicitation, or recommendation of any security or investment product is intended. Certain information and data has been supplied by unaffiliated third parties as indicated. Although Meeder believes the information is reliable, it cannot warrant the accuracy, timeliness or suitability of the information or materials offered by third parties.

Investment advisory services provided by Meeder Asset Management, Inc.

©2023 Meeder Investment Management, Inc.

0116-MAM-8/14/23-36426