You are now leaving Meeder Investment Management. Links to other websites are provided for your convenience and information only. When you click on a link to another website you will be leaving this website. The fact that Meeder Investment Management provides links to other websites does not mean that we endorse, authorize or sponsor the linked website, or that we are affiliated with that website’s owners or sponsors. This material is being provided for informational purposes only and is not a solicitation or an offer to buy any security or to participate in any planning or investment strategy. Unless otherwise indicated, the linked sites are not under our control and we are not responsible for and assume no liability for the content or presentation of any linked site or any link contained in a linked site, or any changes or updates to such sites. We make no representations about the accuracy or completeness of the information contained in any linked sites and their privacy and security policies may differ from ours. We recommend that you review this third-party’s policies and terms carefully.

.png?h=1198&iar=0&w=2274&rev=a3a121a768a34936862087c14535f072&hash=A3B2DEC93CB64A8C64D282597DF14581)

One of the surprising sources of strength in the market has been the jobs market. The unemployment rate has remained stable at 3.6%, while the Labor Force Participation rate ended the quarter around 62.2%. Interestingly, the number of available job openings has reached multi-decade highs, keeping wage pressures high and the outlook for the unemployment rate very well contained around current levels.

» As expected with all the activity in the money market arena, most participants adopted a conservative strategy. Portfolio positioning has moved extremely short with the weighted average maturity (WAM) of most money funds falling from approximately 40 days at the beginning of the year, to under 20 days by the end of the second quarter.

» With the repricing of corporate credit spreads to reflect lower growth and/or recessionary probabilities, we think opportunity remains to selectively add corporate credit exposure to portfolios. The movement in yields and spreads for certain segments of the corporate market will provide an attractive entry point for adding yields not seen in more than a decade, with limited downside risk of further spread deterioration. The challenge will be to determine when to add exposure and in which segments of the sector.

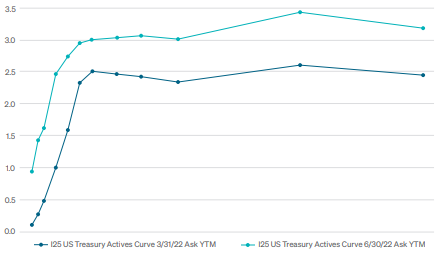

Investment grade spreads typically widen into a recessionary period as balance sheets weaken and purchasing power is lower. The Fed will continue to increase rates until they achieve a neutral level (with Fed Funds at or above the current inflation rate). That type of environment bodes well for diversifying our exposure and following a disciplined duration and spread management approach. The increase in yields is very attractive and locking in higher coupons will be part of our process as we maintain liquidity and utilize a defensive posture.

The views expressed herein are exclusively those of Meeder Investment Management, Inc., are not offered as investment advice, and should not be construed as a recommendation regarding the suitability of any investment product or strategy for an individual’s particular needs. Investment in securities entails risk, including loss of principal. Asset allocation and diversification do not assure a profit or protect against loss. There can be no assurance that any investment strategy will achieve its objectives, generate positive returns, or avoid losses.

Commentary offered for informational and educational purposes only. Opinions and forecasts regarding markets, securities, products, portfolios, or holdings are given as of the date provided and are subject to change at any time. No offer to sell, solicitation, or recommendation of any security or investment product is intended. Certain information and data has been supplied by unaffiliated third parties as indicated. Although Meeder believes the information is reliable, it cannot warrant the accuracy, timeliness or suitability of the information or materials offered by third parties.

Investment advisory services provided by Meeder Asset Management, Inc.

©2022 Meeder Investment Management, Inc.

0116-MAM-7/19/22-26998