You are now leaving Meeder Investment Management. Links to other websites are provided for your convenience and information only. When you click on a link to another website you will be leaving this website. The fact that Meeder Investment Management provides links to other websites does not mean that we endorse, authorize or sponsor the linked website, or that we are affiliated with that website’s owners or sponsors. This material is being provided for informational purposes only and is not a solicitation or an offer to buy any security or to participate in any planning or investment strategy. Unless otherwise indicated, the linked sites are not under our control and we are not responsible for and assume no liability for the content or presentation of any linked site or any link contained in a linked site, or any changes or updates to such sites. We make no representations about the accuracy or completeness of the information contained in any linked sites and their privacy and security policies may differ from ours. We recommend that you review this third-party’s policies and terms carefully.

» U.S. Economic Update

» Fed Meeting in Jackson Hole

» Impact of Rising Rates

» New Asset Requirements for Banks

The U.S. GDP growth rate for the second quarter was revised downward from 2.4% to 2.1%. The revision included more comprehensive data than was available in the first release and showed a decline in private inventory investment. Consumer spending and government consumption continued to increase, but at a lower rate than expected.

The August nonfarm payrolls report exceeded expectations of 170,000 and created 187,000 jobs. Additionally, the unemployment rate unexpectedly rose from 3.5 to 3.8% in August. The increase was primarily due to more job seekers entering the workforce.

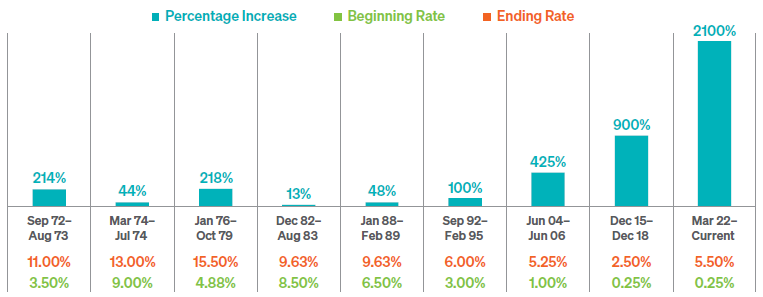

The Fed’s most recent meeting minutes suggest that the committee is near the end of hiking short-term interest rates. According to CME FedWatch, at the end of August, there was a 93% likelihood that the Fed would pause interest rate increases at the September meeting. Meanwhile, the longer end of the yield curve continued to rise as the 10-year U.S. Treasury yield reached 4.3%, its highest level since 2007. Regardless of what the Fed decides on the future of interest rates, the current cycle has already made history as the largest percentage increase when comparing the change from the beginning and ending levels of interest rates.

Commentary offered for informational and educational purposes only. Opinions and forecasts regarding markets, securities, products, portfolios, or holdings are given as of the date provided and are subject to change at any time. No offer to sell, solicitation, or recommendation of any security or investment product is intended. Certain information and data has been supplied by unaffiliated third parties as indicated. Although Meeder believes the information is reliable, it cannot warrant the accuracy, timeliness or suitability of the information or materials offered by third parties.

Investment advisory services provided by Meeder Asset Management, Inc.

©2023 Meeder Investment Management, Inc.

0116-MAM-9/15/23-37144