You are now leaving Meeder Investment Management. Links to other websites are provided for your convenience and information only. When you click on a link to another website you will be leaving this website. The fact that Meeder Investment Management provides links to other websites does not mean that we endorse, authorize or sponsor the linked website, or that we are affiliated with that website’s owners or sponsors. This material is being provided for informational purposes only and is not a solicitation or an offer to buy any security or to participate in any planning or investment strategy. Unless otherwise indicated, the linked sites are not under our control and we are not responsible for and assume no liability for the content or presentation of any linked site or any link contained in a linked site, or any changes or updates to such sites. We make no representations about the accuracy or completeness of the information contained in any linked sites and their privacy and security policies may differ from ours. We recommend that you review this third-party’s policies and terms carefully.

May 2023

April 2023: Capital Markets Commentary

» Fed Update

» First Fed Cut Historically Precedes Equity Weakness

» U.S. Economy Slowing

» Labor Markets

» First Fed Cut Historically Precedes Equity Weakness

» U.S. Economy Slowing

» Labor Markets

Key Takeaways

Fed Update

All eyes were on the May Fed meeting, where the FOMC raised the federal funds rate by +0.25% to 5.25%. It was the 10th hike in this tightening cycle and aligned with market expectations. While the Fed said they have not determined whether to pause future hikes, the Fed removed some language from their statement last meeting and provided more clarity about the outlook for investors. Fed Chair Jerome Powell said, “In determining the extent of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.” The market’s interpretation of this statement was a shift in guidance, indicating the committee might pause future rate hikes and was welcomed by investors.

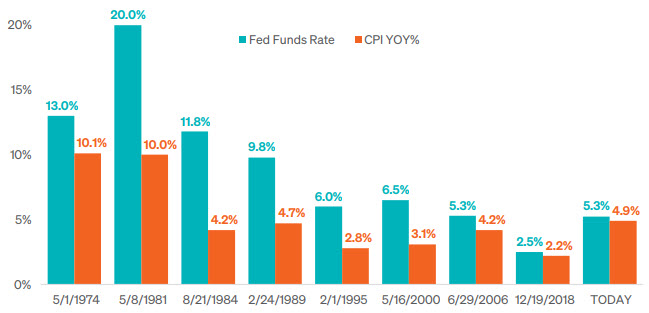

THE FED VS INFLATION

Historically Tightening Cycles End When Fed Funds Rate is Above CPI

SOURCE: STRATEGAS

The timing is significant because it is the first period in this cycle that the Federal Funds rate of 5.25% is now higher than the trailing 12-month year-over year CPI inflation rate of 4.90%. When looking at the past 8 tightening cycles going back to 1974, the Fed did not stop raising interest rates until the Federal Funds rate was higher than inflation.

First Fed Cut Historically Precedes Equity Weakness

It is also important to recognize that although Fed rate cuts are generally seen as a positive for equities, historically it has not happened quickly. When looking over the past 8 tightening cycles, the first interest rate cut has preceded equity weakness. According to Strategas, it took an average of 195 days for the market to reach its low and the S&P 500 Index dropped an average of nearly -24% over this time.

U.S. Economy Slowing

The U.S. economy continues to slow as GDP posted annualized growth of just 1.1% compared to an expectation of 2.0% in the first quarter. This decline was primarily driven by a reduction in business inventories, which is unsurprising as businesses continue to provide weak guidance to investors on their economic expectations. The Leading Economic Index also dropped 1.2% in March to 108.4, reaching its lowest level since November 2020. The ISM manufacturing Index increased slightly to a level of 47.1 but missed expectations of 47.5. The index experienced its sixth monthly contraction in a row. On a positive note, the ISM Services Index increased slightly to 51.9, beating market expectations, and was the fourth consecutive month of expansion. A level above 50 indicates expansion in the industry, where a level below 50 signifies an industry contraction.

Labor Markets

A positive sign is the labor market continues to be unfazed by the dimming economic outlook. Job growth continues to be vibrant as April’s non-farm payrolls increased +253,000 compared to an expectation of +180,000 jobs. This growth was broad-based across industries. The U.S. unemployment rate fell to 3.4%, compared to expectations of 3.6%.

The views expressed herein are exclusively those of Meeder Investment Management, Inc., are not offered as investment advice, and should not be construed as a recommendation regarding the suitability of any investment product or strategy for an individual’s particular needs. Investment in securities entails risk, including loss of principal. Asset allocation and diversification do not assure a profit or protect against loss. There can be no assurance that any investment strategy will achieve its objectives, generate positive returns, or avoid losses.

Commentary offered for informational and educational purposes only. Opinions and forecasts regarding markets, securities, products, portfolios, or holdings are given as of the date provided and are subject to change at any time. No offer to sell, solicitation, or recommendation of any security or investment product is intended. Certain information and data has been supplied by unaffiliated third parties as indicated. Although Meeder believes the information is reliable, it cannot warrant the accuracy, timeliness or suitability of the information or materials offered by third parties.

Investment advisory services provided by Meeder Asset Management, Inc.

©2023 Meeder Investment Management, Inc.

0116-MAM-5/10/23-34243