You are now leaving Meeder Investment Management. Links to other websites are provided for your convenience and information only. When you click on a link to another website you will be leaving this website. The fact that Meeder Investment Management provides links to other websites does not mean that we endorse, authorize or sponsor the linked website, or that we are affiliated with that website’s owners or sponsors. This material is being provided for informational purposes only and is not a solicitation or an offer to buy any security or to participate in any planning or investment strategy. Unless otherwise indicated, the linked sites are not under our control and we are not responsible for and assume no liability for the content or presentation of any linked site or any link contained in a linked site, or any changes or updates to such sites. We make no representations about the accuracy or completeness of the information contained in any linked sites and their privacy and security policies may differ from ours. We recommend that you review this third-party’s policies and terms carefully.

At Meeder Private Wealth we are utilizing separately managed accounts. Unlike a mutual fund where everyone has the same experience, in Private Wealth accounts, the portfolio is built specifically for each client. Each client has control by owning the cost basis on all the underlying positions. With Private Wealth, other investors’ behavior no longer impacts your tax bill. This year the volatility has been high, and the market is down pretty much across the board. This market volatility has presented opportunities for actively tax loss harvesting across our accounts, turning what would be for many, a tax cost into an actual tax benefit. Now is the time to review your accounts that contain mutual funds and ETFs. Because of the market decline, many clients may not have as large of a tax bill to move out of those funds and into a Private Wealth account. Making the move to Private Wealth allows for greater tax control going forward.

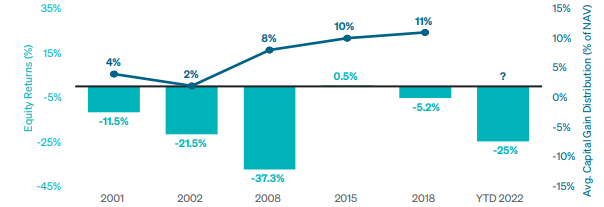

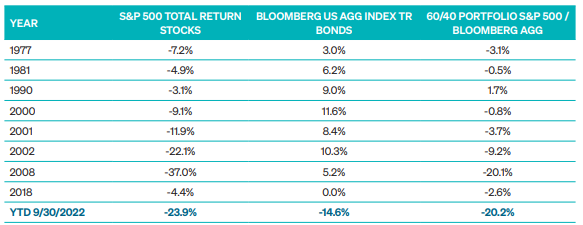

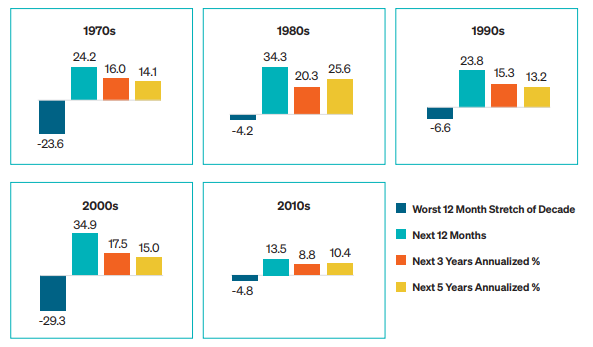

It has been a challenging year for equity and fixed income markets. Since 1977, there have been only 8 down years in the S&P 500. In each of these years where the S&P 500 experienced negative returns, the fixed income market represented by the Bloomberg U.S. Aggregate Index provided diversification and income to offset the equity downside. The challenge this year has been the negative performance of fixed income which has resulted in greater downside participation.

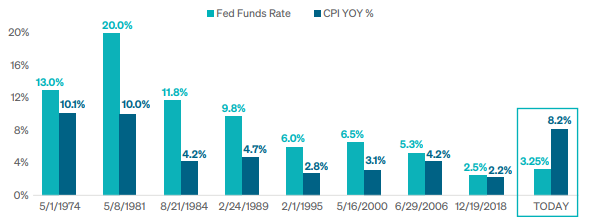

The Fed’s attempt to rein in inflation, remains the number one concern for investors. One way to try and analyze this is to view what the Fed has done from a historical perspective during other rising rate periods. The chart shows the peak Fed Funds rates and inflation represented by CPI year-over-year when the Fed reached the peak rate. If you look back from 1974 to today during the past eight tightening cycles, the Fed did not stop raising rates until the Federal Funds rate was higher than inflation. Today, the Fed Funds rate is at 3.25% and inflation at 8.2%. It is likely that interest rates will continue to climb and peak at a level above CPI.

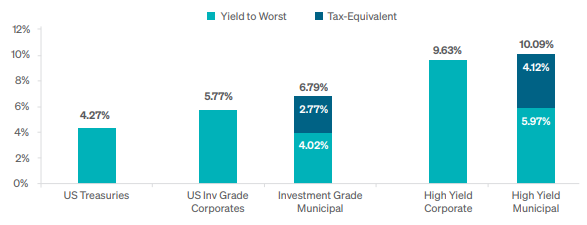

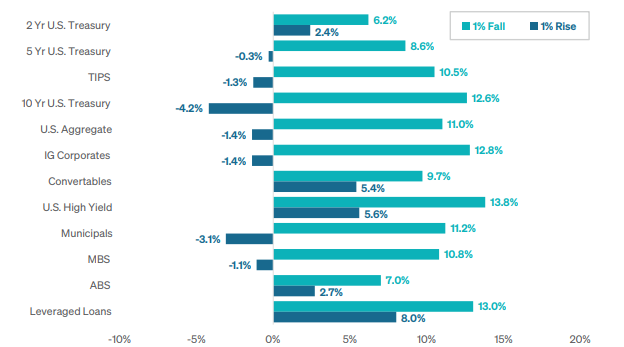

Below are the yields across several core investments as well as high yield. U.S. Treasuries are yielding over 4%, investment grade corporates nearly 6% and investment grade municipals nearly 7% for your clients in the highest federal tax bracket. We are finding core investments very attractive today. We maintain a high yield allocation, but we would argue that there may be a better buying opportunity in the future. High yield has held up very well given the equity weakness. Should we see additional credit stress, there may be a better a buying opportunity which we will be equipped to capture.

For risk management we take a holistic approach; we want to know as much about each client’s financial situation as possible. The more information we have about their entire financial picture the more effectively we can manage their investments and ensure we are maintaining their specific risk profile. We can manage around concentrated positions, excluding stocks, sectors, or industries. All this information can be considered and allows our team to build the portfolio to be as effective and efficient as possible while maintaining the agreed-upon risk profile.

An area that we would consider to be one of the most underserved from a portfolio management standpoint is tax management, which often represents a large part of our conversations with advisors and clients. We implement active and ongoing tax-loss harvesting, as well as gain deferral when needed. The tax loss harvesting isn’t simply selling stocks that are down at the end of the quarter or the end of the year. This is a more thoughtful approach where every account is reviewed daily to determine if there are opportunities within the portfolio to harvest losses. This active tax management allows us to maximize after-tax wealth for our clients and generate tax alpha.

Finally, this is a transparent and unbiased approach. While Meeder does offer a full suite of mutual funds, we do not use any proprietary products inside of private wealth. Also, the clients will always be able to see in real-time the positions that are being held in the account, along with access to our investment team as needed to answer any questions that may arise.

Commentary offered for informational and educational purposes only. Opinions and forecasts regarding markets, securities, products, portfolios, or holdings are given as of the date provided and are subject to change at any time. No offer to sell, solicitation, or recommendation of any security or investment product is intended. Certain information and data has been supplied by unaffiliated third parties as indicated. Although Meeder believes the information is reliable, it cannot warrant the accuracy, timeliness or suitability of the information or materials offered by third parties.

Investment advisory services provided by Meeder Asset Management, Inc.

©2022 Meeder Investment Management, Inc.

0183-MAS-10/26/22-28064