You are now leaving Meeder Investment Management. Links to other websites are provided for your convenience and information only. When you click on a link to another website you will be leaving this website. The fact that Meeder Investment Management provides links to other websites does not mean that we endorse, authorize or sponsor the linked website, or that we are affiliated with that website’s owners or sponsors. This material is being provided for informational purposes only and is not a solicitation or an offer to buy any security or to participate in any planning or investment strategy. Unless otherwise indicated, the linked sites are not under our control and we are not responsible for and assume no liability for the content or presentation of any linked site or any link contained in a linked site, or any changes or updates to such sites. We make no representations about the accuracy or completeness of the information contained in any linked sites and their privacy and security policies may differ from ours. We recommend that you review this third-party’s policies and terms carefully.

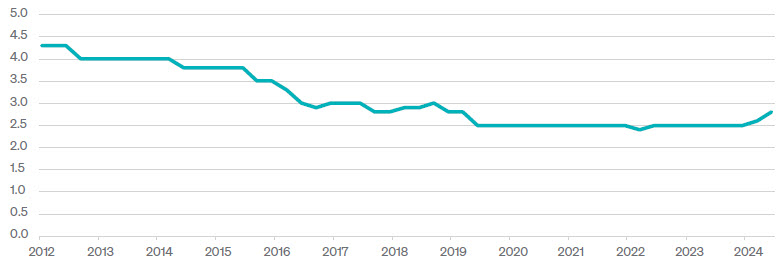

The Fed’s preferred inflation gauge, Core PCE (Personal Consumption Expenditures Price Index), which peaked at 5.57% in February of 2022, dropped in July to 2.62% year-over-year. Another commonly followed inflation index, the CPI (Consumer Price Index) also fell from a high of 9.10% in June of 2022 to its current level of 2.50%. The Fed’s long-term goal is to keep the level of inflation at or around 2.00% and the recent decline toward that level has given it confidence that it can indeed begin to cut rates.

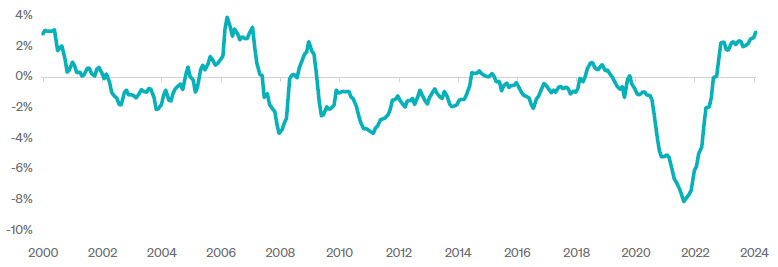

Looking at the real Fed Funds rate (a measure of the Fed Funds rate minus inflation) confirms its beliefs. As the graph below shows, the Fed’s current rate stance is as restrictive to economic growth as it has been in nearly two decades. Beginning a rate cut cycle and easing monetary conditions is likely warranted as current policy is not only restrictive, but inflation has also fallen significantly.

Investment advisory services provided by Meeder Asset Management, Inc.

©2024 Meeder Investment Management, Inc.

0274-MAM-9/13/24-45282